Several recent events brought to mind the issue of performance/reporting standards.

My good friend at Privcap, David Snow recently remarked in an August PrivCap Digest article “Will relaxed rules on general solicitation mean tighter performance reporting requirements”. His point was that with general solicitation now a reality for private equity firms, would/should there be a call for more rigorous standardization and/or transparency in performance reporting.

Recently, a firm–TopQ—founded by industry veterans formerly from SL Capital Partners launched www.topquartile.com to provide GPs with online tools to distribute their track records to prospective investors and to calculate their returns on a daily cashflow basis because ostensibly, a lot of GPs calculate their returns on a monthly or quarterly cashflow basis which is a no-no in this day and age of advanced database and accounting technology and because there is/can be a demonstrable and material difference in compounding effects between calculating returns on a monthly, quarterly or daily basis. In addition they propose you examine an entire firm’s track record rather than cherry-picked funds.

Thirdly, an effort launched by eFront and some of its clients and close relationships created the AltExchange Alliance which is a consortium to standardize the taxonomies used to transfer transactions ,demographic data, and related entity information. It doesn’t currently provide standards for performance reporting but I would suspect that has to be on the roadmap.

These standards already exist

I am going to take off my agnostic hat off for a little bit because the standards and industry practices called for above already exist. The Global Investment Performance Standards (GIPS) created and promulgated by the CFA institute is a series of guidelines which require and recommend exactly what many in the industry are asking for—a rigorous set of guidelines for standardized returns and performance reporting. These standards were written by industry practitioners and reviewed and promulgated by an independent body.

Full disclosure: I fortunate have the privilege to chair the private equity working group that drafted the most recent GIPS guidelines. I’ve also been a member of the working group since 1994.

Much has been written about GIPS both in the general financial press and the private equity press since their official release in 2006 but a redux is in order since it hasn’t been in the news lately and the aforementioned events warrant a reminder.

There is no way to do justice to the full extent of GIPS in this short article so we offer a brief recap.

A bit of background

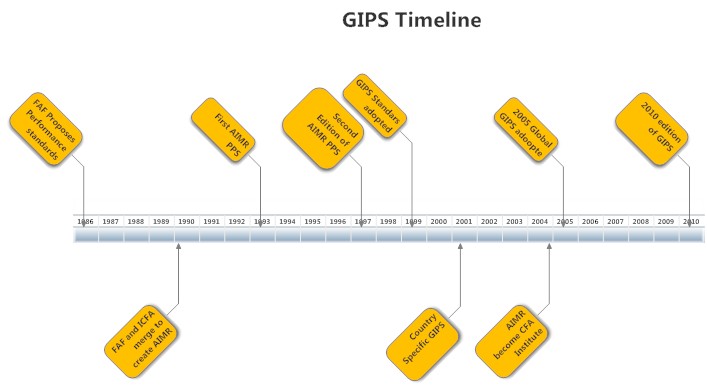

AIMR introduced the first Performance Presentation standards in the 1990s to provide guidelines in how investment managers of all types report their performance to prospective investors.

According to the foreword of the 1993 AIMR Performance Presentations Standards, the presentation standards were first introduced In the September/October 1987 issue of the Financial Analyst Journal under the auspices of the Financial Analysts Federation (FAF). They were discussed, reviewed and revised substantially in the subsequent years. In 1990 the Financial Analysts Federation and the Institute of Chartered Financial Analysts were joined together to form the Association for Investment Management and Research (AIMR). AIMR endorsed and approved the aforementioned standards and implemented them as the AIMR performance presentation standards in 1993. There was a second edition of the AIMR PPS released in 1997.

Subsequently the AIMR performance presentation standards became GIPS in 1999 and AIMR became the CFA institute in 2004. By 2005 the various country-specific versions of the presentation standards were merged to create a global set of standards which is now called GIPS.

The most recent version of GIPS was released in 2010 effective January 1, 2011.

The guidelines provide the mainstream and alternatives asset classes with standards on presenting performance analysis to prospective investors. The intent is to provide prospective investors with an apples-to-apples comparison of pure and attributable performance track records for investment managers, their vehicles and firms with commensurate disclosure and transparency.

So how does this affect the private equity industry?

In the first edition of the standards issued in 1993, the AIMR-PPS issued the following requirements:

- Total returns including realized and unrealized gains and losses plus income are required.

- Time weighted rate of return is required using a minimum of quarterly valuations and linking of these interim returns.

The following were recommendations:

- Gross returns are recommended.

- Daily valuations are recommended

As you can imagine, these requirements didn’t sit well with venture capital, real estate, private equity and other asset class participants long ensconced in the internal rate of return or money weighted rate of return, net returns to investor theology. In addition, daily valuations for the aforementioned asset classes are were a pipe dream. After the backlash from practitioners in the private equity and real estate industries, AIMR’s next version sought to address these asset class-specific performance presentation issues.

To make the standards more relevant to alternative asset classes, AIMR created a venture capital and private placement subcommittee in 1995 as well as other relevant subcommittees for other asset classes and has had a similar subcommittee/working group for every revision since the second edition.

Industry-led performance presentation guidelines

Unlike some standards, where various advisors and organizations “endorse” those guidelines and standards, the AIMR/GIPS guidelines were drafted by its subcommittee members during a intensive and rigorous editing, revision and comment cycle over a period of several months.

The private equity sub-committee has always been made up of industry practitioners. For the second edition of the AIMR PPS issued in 1997, the inaugural venture capital and private placements sub-committee committee members included::

- General Motors–R. Charles “Chuck” Tschampion and Bill Miller

- Brinson Partners now called Adams Street–Bondurant (“Bon”) French

- Cattanach and Associates –Gail Marmonstein Sweeney

- State Street Bank and Trust Co.–Paul Price.

- Myself

For the 2005 edition of what was now known as GIPS, the private equity subcommittee members included:

- Pantheon Ventures (Chair)–Carol Kennedy

- State Street –Scott Brown

- OMERS –Lynn Clark

- 3i Ventures–Patrick Cook,

- CALPERS -Rick Hayes

- JAFCO -Shinji Koga

- Robeco -Ad van den Ouweland

- Ennis Knupp/Mercer–Nancy Williams

- JP Morgan Fleming Asset Management–Iain McAra

- ILPA (observer)-Arlett Tygesen

- Myself

In its latest revision of 2010 the members of the GIPS committee included:

- Myself (Chair)

- Alignment capital–Austin Long, Craig Nickels

- Patheon Ventures–James Haworth

- NVCA-represented by Louis Sciarretta of Flag Capital

- EVCA–Mirela Ene

- BVCA—Dr. Mei Nui

- Robeco–Ad van den Ouweland

- Pathway capital–Milt Best

- Adams Street–Raymond Chan

- Cambridge Associates–Rik Neunighoff

- JAFCO-Tetsuro Higuchi

- Burgiss Group–James Bachman

Over the years, this august group has been deeply committed to creating the most rigorous standards possible to fairly and accurately presenting performance for the private equity industry especially when compared to other asset classes which are also GIPS-compliant.

GIPS is PE-Friendly with Limited Partners being top of mind

Without going into great detail (the guidelines and its attendant FAQs, interpretative guidance and related materials run into hundreds of pages compared with the 1993 edition which consisted of only 73 pages) – the highlights of the private equity related guidelines stipulate either by requirement or recommendation:

- Returns be calculated on a net-to-investor basis

- Returns are not presented just for investment vehicles but presented firm-wide

- That relevant fees/expenses be deducted in calculating and presenting returns and performance

- Returns be calculated on a internal rate of return basis as well as calculating the normative DPI, RVPI, TVPI multiples

- Returns can be compared to public markets using any of the available public market equivalent methodologies (PME) with requirements to disclose which method and public market indexes were used.

- Prohibits an investment firm from cherry picking which funds to disclose to prospective investors.

- All vehicles must be in a “composite”

- Valuations must be presented on a fair value basis.

- Basic “composite” is the “vintage year”

- Cashflows must be calculated on a daily basis.

- There are a series of required and recommended disclosures which provide much-needed transparency.

In the 2010 edition, there are specific guidelines for fund of fund managers and semi-captive groups that were not addressed in the 2005 or previous editions.

These are fairly standard industry practices so there aren’t many surprises here, but it does codify in rigorous detail how returns and performance should be reported and presented to prospective investors.

As a result this is probably the most comprehensive set of industry performance reporting standards in existence and as they were created by industry practitioners themselves using the most commonly accepted industry methods for performance calculation, reporting and disclosure, they should provide more than adequate disclosure necessary to fully inform investors.

Are there any caveats?

Like any body of knowledge, there is always a need for improvement. Otherwise there would be no reason for a 1993 edition, 1995 edition … 2005 edition, 2010 edition etc.

From my perspective, users of the GIPS guidelines should note the following caveats among others:

- It is meant to apply only to investment managers reporting returns and performance to prospective investors, not to current investors.

- It is not meant to apply to limited partners reporting their performance. – we’ll cover that in an entire different series of future articles.

- As well known as the CFA institute is, and as well-promulgated GIPS has been, there is still not a ubiquitous adoption by name in the private equity industry, although many GPs follow the spirit or intent or even the letter of the guidelines without knowing it.

We hope to continue to improve the guidelines and improve adoption, but first, practitioners need to be aware of the guidelines and know that they follow accepted practices.

I would propose that we don’t need more standards – simply apply or improve the standards that exist. GIPS goes a long way towards fulfilling the needs of investors with transparent and rigorous track record reporting.

Thoughts? – leave a comment

Can you also comment on risk measurement for PE funds. is VAR even applicable for a PE fund?

Look for for a whole series of upcoming content articles on private equity risk. There is a lot of academic and practitioner research on the topic but no one methodology has emerged as mainstream.

VAR is not really a good measure as VAR depends so much on “marked to market” valuations. In many markets that depend on the public markets, market prices provides a contemporaneous valuation thus you can create a probability distribution on loss based on the market price at any point in time.

“Pricing”/valuation of private equity funds is not contemporaneous and its volatility is typically attenuated because the valuations tend to be appraisal valuations rather than market based valuations thus there isn’t a direct analog to VAR that would be commensurable.

There are other measures that have been researched that work a bit like VAR but the only comparison you could make would be against other private equity funds. You couldn’t use them to compare private equity risk to a public equity asset manager.